Saturday, June 29, 2013

Thursday, June 27, 2013

Government Motors (GM) to Invest $691 Million in Mexico

Monday, June 24, 2013

You Think Now is a Good Time to Buy That House Because Rates Are So Low -- Well, You Better Think Again!

Realtors love to claim that today's low interest rate environment is the best time to purchase your dream home. Well, I contend that propaganda from realtors

will lead directly to your next nightmare.

So here is the economic reality from Wells Fargo, in which the national

average 30-year Fixed Mortgage has gone from 3.40% on May 1, 2013 to 4.875%, as

of today. The matching affordability

collapse (See the following graph.) has gone from $450,000 to $375,000, or a 16%

equilibrium price drop in under two months!

What

this graph definitely illustrates, absent an increase in disposable

income, is the average home affordability plunges as rates go

up; and, of course, the value of your home declines!

Saturday, June 22, 2013

Questions That American Taxpayers Would Like to Know the Answers

Friday, June 21, 2013

Tuesday, June 18, 2013

The Mandate of the Federal Reserve System

"The

Board of Governors of the Federal Reserve System and the Federal Open

Market Committee shall maintain long run growth of the monetary and

credit aggregates commensurate with the economy's long run potential to

increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates." Now, stable is defined as not subject to sudden or extreme change or fluctuation. With that definition in mind, let's see how the Federal Reserve System has performed since 1913 in regard to its goal of stable prices.

A dollar in 1913 would be worth only four cents today, or it has lost 96% of its value. (So much for stable prices!)

In other words, its performance on stable prices has been a complete disaster. Why the comparison with 1913? That is the year of the birth of the

Federal Reserve System. Therefore, my recommendation would be to eliminate the

Federal Reserve System, which is based on a fiat currency, and replace

it with a sound currency system, such as gold. See, the Federal Reserve

System can inflate, create, as many dollars as they want without

anything backing those dollars. By the way, that is what we mean by

monetary inflation, which must be distinguished from price inflation.

Price inflation is the rise in the prices we pay for goods and services.

Price inflation is caused by monetary inflation, which is solely

controlled by the Federal Reserve System. That is why monetary inflation is so insidious, because it may take years before it shows up as price inflation.

Don't expect Congress to make the Federal Reserve System accountable for its utter failure to defend the stability of the dollar. Why? Because Congress is as complicit and culpable as the Federal Reserves System. If it wasn't for the Federal Reserve System providing the trillions of dollars to finance the federal deficits year after year, Congress would not be able to deficit spend. And, therein lies why Congress is complicit and culpable to the actions of the debasement of the dollar by the Federal Reserve System.

Monday, June 17, 2013

You've Lost That Loving Feeling

Back on September 13, 2012, my post, which was entitled, "And the Winner of the 2012 Presidential Election Is?" made the following statement: (Pay close attention to the last sentence.)

"Underlying social mood as manifested in the stock market remains

positive going into the November election.

Therefore, the probability of President Obama being re-elected is high! So, how can one use the above information against

the backdrop that the next four years will usher in the largest

economic/financial disaster known to man with the DJIA selling for 1,000? (Yes, the coming economic downturn will be

greater than the Great Depression of the 1930s.) Given the scenario, I don’t consider who ever

occupies the White House will win any popular contests. Remember that over the next four years the

expected social mood of this country will change from positive to very

“bleak.” Therefore, the man that

occupies the Presidency will undoubtedly be highly despised."

Here we are eight months into President Obama's second term, and his popularity has drastically shifted against him. CNN reports that for the first time in his presidency, half of the public doesn't think that Barack Obama is honest and trustworthy. So far into his second term, we have had one scandal after another -- "Associated Press, IRS, Unwarranted Electronic Surveillance of U.S. Citizens, and Benghazi." And, this is after only eight months. So, the trend change in social mood for President Obama and Wall Street is only going to get much worse. In regard to Wall Street, the manipulation of financial assets (stocks and bonds) by the Federal Reserve System will end in disaster over the next three years, specially the date to watch is September 13, 2015. (See my post of November 19, 2012 by clicking here for the reason why September 13, 2015 is significant.)

Tuesday, June 11, 2013

Forget Gold and Silver, Buy Ammo!

Since May 2012, 22 ammunition is up over 400%. It was approximately $21 to $23 per 500 rounds (full brick) in May 2012, and it is now $100 to $135 for 500 rounds, if you can find it. Over the same time period, gold and silver are down approximately 15% and 27%, respectively. So what we have in place is a de-facto gun control in the United States. That is, one can buy all the guns one wants; however, buying the ammo for those guns is another matter! Therefore, if one does not have the ammo for one's gun, what good is it?

Monday, June 10, 2013

Too Good to be True, But This is True!

Tuesday, June 04, 2013

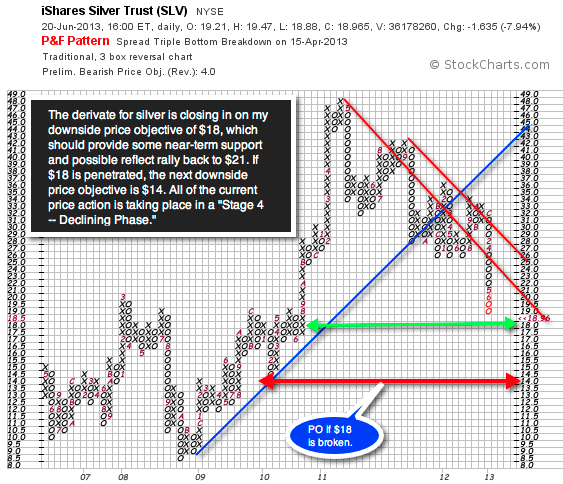

$SLV (Derivative for Silver) Update

Nothing has really changed on my outlook for $SLV. My downside target is still in the $18 to $20 range. From my "Stage Analysis Approach," $SLV continues at Stage Four, which is the selling phase, or that phase were supply is greater than demand.

Subscribe to:

Posts (Atom)